Bangladesh might have experienced capital flight in the last financial year evidenced from the unusual outflow of funds as well as unrealised export proceeds, said the International Monetary Fund (IMF).

It said foreign currency shortages and letter of credit margin requirements on the payments by bank deposits to curb non-essential imports led to a sharp contraction in imports by 16 percent in FY23.

Exports remained resilient, despite slow growth in major trading partners. The current account balance improved significantly.

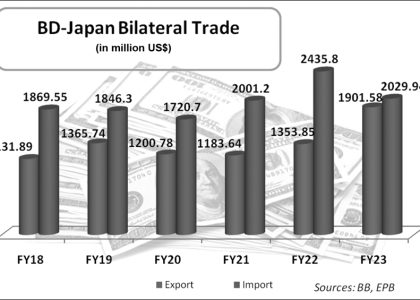

While the total shipment value of exports from the Export Promotion Bureau recorded under the BoP grew by 6.3 percent year-on-year in FY23, the receipts recorded by the Bangladesh Bank based on forex deposits at commercial banks increased marginally relative to FY22.

Consequently, unrealised export proceeds — the difference between export shipments and realised export proceeds — increased to $9.6 billion, which amounted to 2.1 percent of GDP in FY23. This reflected delayed repatriation and repayment of export proceeds, turning short-term trade credit sharply negative, the paper said.

High global inflation and continued supply disruptions have increased import costs for externally financed investment projects, resulting in delayed project execution, and consequently reducing corresponding external project finance disbursements.

Historically the financial account of Bangladesh has experienced a surplus almost every year.

In a footnote, the IMF said while some share of the gap can be attributed to “local exports” (shipments from export processing zones to domestic market mistakenly attributed to exports) and export payment cancellations due to quality control issues and vendor bankruptcies, historically high unrealised export proceeds signal capital flight.

“Uncertainty around general elections could also be another near-term contributing factor to high levels of unrealised export proceeds, as exporters reportedly choose to withhold bringing their proceeds back into the country until the results of the election are finalised,” the IMF said.

The latest figures of the funds that went out of the country through illegal means were unavailable.

In December 2021, the Global Financial Integrity, a Washington-based organisation, said Bangladesh lost approximately $8.27 billion on average annually between 2009 and 2018 from mis-invoicing of values of import-export goods by traders to evade taxes, and illegally move money across international borders.

Speaking to The Daily Star yesterday, Zahid Hussain, a former lead economist of the World Bank Bangladesh, said the IMF has merely skimmed the surface. “It could give further details on the subject.”

The IMF report said faster-than-anticipated global monetary policy tightening, inadequate domestic policy response, and expectation of further currency depreciation have contributed to financial outflows. The policy rate gap between Bangladesh and the US declined from 4.9 percent at the start of the pandemic to 1.2 percent by end-June 2023.

At the same time, inflation remains elevated leading to a widening inflation gap with the US. As Bangladeshi firms reduced foreign borrowing, private external credit inflows declined sharply.

Net short-term private loan inflows of $3.1 billion in FY22 reversed to an outflow of $1.9 billion in FY23, as repayments outpaced new loans due to higher global financing costs.

In addition, frequent changes to exchange rate policy setting, uncertainty surrounding the forex management framework and expectation of further currency depreciation have added to significant delays in export repatriation.

To address the repatriation delays, the BB in March 2023 mandated that export receipts would be converted at the exchange rate prevailing on the market on the date when the proceeds should have been realised.

The IMF said transitioning to greater exchange rate flexibility could incur adjustment costs. Moreover, disorderly transitions could result in sharp depreciations or exchange rate overshooting if not accompanied by an appropriate monetary and fiscal policy stance.

Lack of developed forex markets, appropriate intervention policy, technical capacity to adopt an alternate nominal anchor, and monetary policy independence have resulted in short-lived but ultimately unsustainable attempts to adopt flexible exchange rate regimes in some countries.

According to the paper, quantifying these adjustment costs remains challenging in Bangladesh.

First, the net negative impact on the budget stemming from increased external debt servicing costs and higher implied fiscal subsidies for imported essentials (including food, energy, and other commodities) could be substantial.

External debt service, which stood at around 1 percent of GDP for FY23, and fiscal subsidies for natural gas, electricity, fertilizers, and food, which amounted to 1.4 percent of GDP in FY23, would rise further with depreciation, the latter, especially given the absence of automatic domestic price adjustment mechanism.

Second, the passthrough from depreciation could contribute to an increase in prices, it said.

According to the IMF, a more flexible exchange rate regime is essential for Bangladesh to rebuild external resilience and successfully integrate into the global financial system post-LDC graduation.

“Near-term policy actions should adopt a tight monetary stance and maintain fiscal discipline to support a move toward greater exchange rate flexibility.”

It says the BB should adopt a transitional exchange rate arrangement, reducing the reliance on the exchange rate as the primary nominal anchor, and gradually moving to a credible inflation target as a sole nominal anchor for monetary policy.

The transitional exchange rate arrangement could involve a gradual shift from a single reference currency peg to a basket of currencies with a narrow band corridor. Gradually increasing flexibility through wider exchange rate bands would develop a better awareness of forex risks among market participants.

Zahid Hussain opposed IMF’s suggestion regarding the transitional exchange rate arrangement.

“The transitional exchange rate is a long process. The IMF has talked about some impacts. What the IMF has not said is that Bangladesh is already facing the cost stemming from the delay in leaving the exchange rate in the hands of the market.”

“But if we can bring in the reform, the supply of US dollars will increase in the market.”

Owing to a lack of reform, inflation has surged to record levels while the payments to independent power producers can’t be made on time, Hussain said.